Economists watch oil.

Politicians watch groceries and rent.

Markets watch the Fed.

Everyone is watching gas and diesel prices.

But buried deep inside a relatively obscure U.S. Bureau of Labor producer-price series may be an entirely different inflation story — one that could define the next decade of enterprise economics.

The number is semiconductor and electronic component producer pricing .

And it may be flashing a warning that almost nobody is talking about.

The Data Nobody Is Looking At

The producer price index for semiconductors and electronic components is most easily accessed through the Federal Reserve Bank’s FRED® platform (series ID PCU3344133441). Upon review, the data looked almost boring through most of 2025.

For months, prices barely moved. Then something changed. By August 2025, prices began climbing. By early 2026, they exploded.

reserve obs get PCU3344133441 --start 2024-01-01 --end 2026-05-01 --format jsonl | reserve transform resample --freq monthly --method mean | reserve chart bar

PCU3344133441 2024-01 – 2026-04

2024-01 57.88 ██

2024-02 58.05 ██

2024-03 58.1 ███

2024-04 58.26 ███

2024-05 58.2 ███

2024-06 58.06 ██

2024-07 57.46 █

2024-08 57.49 █

2024-09 57.54 █

2024-10 58.0 ██

2024-11 58.94 ██████

2024-12 58.83 █████

2025-01 58.27 ███

2025-02 58.07 ██

2025-03 58.42 ████

2025-04 58.32 ███

2025-05 58.33 ███

2025-06 57.61 █

2025-07 57.58 █

2025-08 59.64 █████████

2025-09 59.77 █████████

2025-10 60.12 ███████████

2025-11 60.87 ██████████████

2025-12 61.06 ██████████████

2026-01 61.58 ████████████████

2026-02 66.99 ██████████████████████████████████████

2026-03 68.21 ███████████████████████████████████████████

2026-04 73.48 ████████████████████████████████████████████████████████████████

Source: Bureau of Labor Statistics via FRED

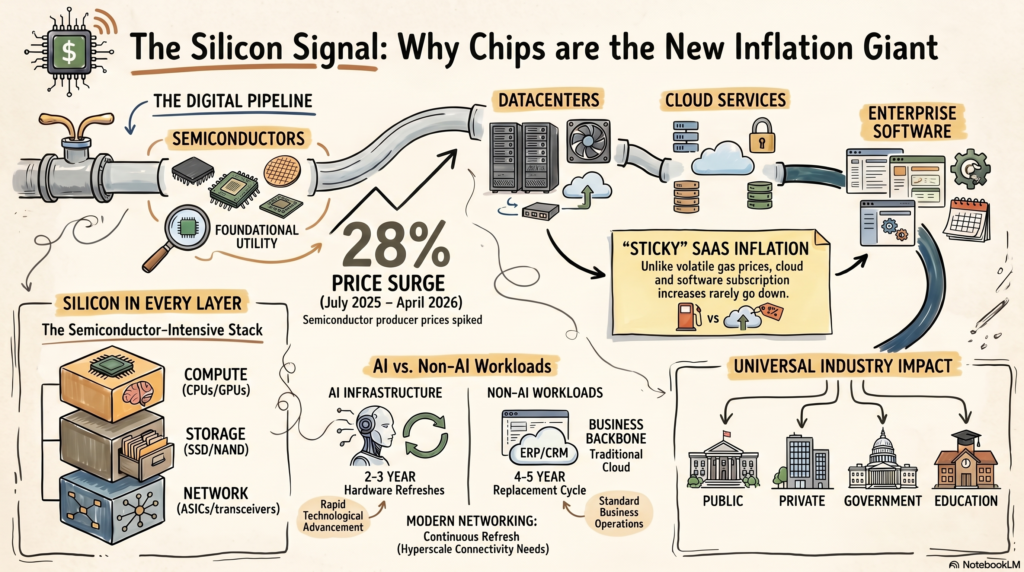

From the July 2025 low to April 2026, semiconductor and electronic component producer prices surged nearly 28%.

That is not the kind of inflation shock typically tied to oil tankers drifting through the Strait of Hormuz or temporary commodity volatility. It is a structural repricing event — one most observers would immediately attribute to the AI gold rush. And they are probably partially correct.

But the implications may reach far beyond AI accelerators themselves.

Semiconductors are no longer just components inside consumer electronics. They are rapidly becoming the foundational infrastructure layer beneath cloud computing, enterprise software, logistics systems, financial platforms, industrial automation, and increasingly the broader economy itself.

If the economics of compute are changing, then the inflation story may be changing with them.

Economists May Be Looking in the Wrong Place

Traditional inflation models were built around industrial-era economics. The classic inflation pipeline looked like this:

Energy -> Transportation -> Manufacturing -> ConsumersThat framework makes sense for a physical economy dominated by: fuel, shipping, factories, and commodity production. But the modern economy runs on something else. Increasingly, the real pipeline looks like this:

Semiconductors & Electronics -> Datacenters -> Cloud Services -> Enterprise Software -> Every IndustryThis is the inflation architecture of a digital economy. And it changes everything.

Compute Has Become a Foundational Industrial Input

For decades, technology was deflationary. Compute, storage, and bandwidth consistently got cheaper. Infrastructure as a Service (IaaS) and Software as a Service (SaaS) promoted lower total cost of ownership and operational efficiency as core selling points. In many cases that promise proved true. In others, it simply shifted costs from internal IT departments into recurring vendor contracts.

What the broader cloud industry unquestionably established, however, was the normalization of annual price increases embedded inside multi-year customer commitments.

For years, none of this appeared dangerous because the underlying economics of technology remained deflationary. The market internalized the idea that technological progress naturally lowers costs over time.

But what if that assumption is beginning to break?

Part of the answer may lie in how the architecture of cloud infrastructure itself has changed.

Historically, the industry treated compute, storage, and bandwidth as distinct infrastructure categories:

- compute meant CPUs and servers,

- storage meant hard drives and storage arrays,

- bandwidth meant fiber and networking equipment.

Today, all three increasingly collapse into one semiconductor and electronic component intensive stack.

Compute is obviously driven by CPUs, GPUs, accelerators, and memory. But storage is now dominated by NAND flash and SSD controllers. Even bandwidth is no longer “just fiber.” Modern hyperscale networking depends on switching ASICs, optical transceivers, packet processors, NICs, DSPs, and routing silicon. The intelligence layer of the modern internet is semiconductor-driven.

The result is that cloud infrastructure has quietly become an enormous assembly of semiconductor and electronic component based systems connected by glass.

And cloud infrastructure is no longer a niche industry. It is becoming the operational backbone of the global economy.

Payroll systems, logistics platforms, ERP software, CRM systems, healthcare infrastructure, and financial platforms now run inside hyperscale datacenters. These are not speculative AI workloads. They are ordinary, everyday business operations that increasingly depend on semiconductor-intensive infrastructure.

This matters because hyperscalers are entering a perpetual hardware replacement cycle.

That is why a sustained rise in semiconductor and electronic component producer prices matters. If these input costs remain elevated — or continue rising — the effects will eventually work their way through the cloud stack itself, placing upward pressure on SaaS, IaaS, AI inference, and enterprise software pricing.

Not immediately. Hyperscalers hedge aggressively, negotiate long-term supply contracts, and amortize infrastructure investments over years. But producer-price inflation at the hardware layer rarely disappears permanently. Eventually, it surfaces somewhere in the economics of the digital economy.

The Economics Nobody Wants to Talk About

When people discuss AI infrastructure, they focus on model capabilities.

But the economic story is much larger. Google Cloud recently reported:

- $20 billion in quarterly revenue,

- 63% year-over-year growth,

- A staggering $462 billion contract backlog

That backlog may be the most important number.

Why?

Because it signals that corporations are committing themselves to long-duration cloud dependence.

These are not experimental workloads or simple eliminations of “server closets” anymore. Cloud infrastructure is becoming mandatory infrastructure. And mandatory infrastructure eventually gains pricing power.

The Replacement Cycle Problem

The semiconductor story becomes even more interesting once you examine hardware replacement cycles. Traditional enterprise servers were typically replaced every 4–5 years. That cycle roughly holds true for the racks of compute infrastructure that powers IaaS and SaaS offerings. AI infrastructure may need replacement every 2–3 years — possibly even faster. The result has been and will continue to be growing and persistent semiconductor demand. Not cyclical demand. Not temporary demand. Permanent demand.

What Happens If Compute Stops Being Deflationary?

This is the macroeconomic question sitting quietly beneath the surface of the semiconductor data. What happens if compute itself becomes inflationary?

The Bureau of Labor Statistics has been tracking Semiconductor as a separate price index since 1984. For those who lived it, you remember the story as prices came down and the economy digitized. The financial crisis of 2008 did not have material impact nor did the post COVID recovery era.

reserve obs get PCU3344133441 --start 1984-01-01 --end 2026-04-30 --format jsonl | reserve transform resample --freq annual --method mean | reserve chart bar

PCU3344133441 1984 – 2026

1984 100.0 ████████████████████████████████████████████████████████████

1985 100.5 █████████████████████████████████████████████████████████████

1986 102.4 ███████████████████████████████████████████████████████████████

1987 102.6 ███████████████████████████████████████████████████████████████

1988 104.0 █████████████████████████████████████████████████████████████████

1989 105.1 ███████████████████████████████████████████████████████████████████

1990 104.9 ██████████████████████████████████████████████████████████████████

1991 104.9 ██████████████████████████████████████████████████████████████████

1992 104.6 ██████████████████████████████████████████████████████████████████

1993 105.3 ███████████████████████████████████████████████████████████████████

1994 104.8 ██████████████████████████████████████████████████████████████████

1995 102.6 ███████████████████████████████████████████████████████████████

1996 99.31 ███████████████████████████████████████████████████████████

1997 95.13 ██████████████████████████████████████████████████████

1998 91.85 █████████████████████████████████████████████████

1999 90.09 ███████████████████████████████████████████████

2000 88.76 █████████████████████████████████████████████

2001 86.38 ██████████████████████████████████████████

2002 84.86 ████████████████████████████████████████

2003 81.08 ███████████████████████████████████

2004 78.27 ███████████████████████████████

2005 76.49 █████████████████████████████

2006 75.14 ███████████████████████████

2007 70.2 █████████████████████

2008 66.27 ███████████████

2009 65.39 ██████████████

2010 63.86 ████████████

2011 61.55 █████████

2012 59.52 ██████

2013 59.23 ██████

2014 58.77 █████

2015 58.38 █████

2016 57.33 ████

2017 56.81 ███

2018 55.98 ██

2019 55.34 █

2020 54.77 █

2021 54.66 █

2022 56.86 ███

2023 57.19 ███

2024 58.07 █████

2025 59.0 ██████

2026 67.57 █████████████████

Source: Bureau of Labor Statistics via FRED

Enter late 2025 and the start of 2026 and semiconductor returns to mid-2000 levels as if it went through an overnight time machine! The difference is that the number of business critical corporate and government workloads that have been migrated to the cloud in the last 20 years has been exponential.

To net it out, rising semi-conductor costs lead to rising cloud infrastructure cost. These costs are the inputs that will drive up SaaS software operating costs and find their way financials just about every sector of the economy both private and public.

The result is a new kind of inflation transmission mechanism. This will not taking place through gasoline pumps but through recurring software invoices. And unlike commodity spikes, SaaS inflation is sticky. Once enterprise subscription pricing rises, it rarely falls.

The New Inflation Utility

Electricity became a universal industrial utility in the 20th century. Compute may be becoming the equivalent utility of the 21st century. If so, semiconductors are no longer just components. They are upstream economic infrastructure. Which means semiconductor pricing may increasingly behave less like a cyclical technology sector and more like a foundational inflation input.

That possibility is hiding in plain sight inside the producer-price data. Yet, the news headlines are still talking about the price of diesel. The next inflation giant may already be sitting quietly inside the datacenter.